2 - Regression Diagnostics

Outline

2.0 Regression Diagnostics

2.1 Unusual and Influential data

2.2 Tests on Normality of Residuals

2.3 Tests on Nonconstant Error of Variance

2.4 Tests on Multicollinearity

2.5 Tests on Nonlinearity

2.6 Model Specification

2.7 Issues of Independence

2.8 Summary

2.9 For more information

2.0 Regression Diagnostics

When run regression models, you need to do regression disgnostics. Without verifying that your data have met the regression assumptions, your results may be misleading. This section will explore how to do regression diagnostics.

- Linearity - the relationships between the predictors and the outcome variable should be linear

- Normality - the errors should be normally distributed - technically normality is necessary only for the t-tests to be valid, estimation of the coefficients only requires that the errors be identically and independently distributed

- Homogeneity of variance (homoscedasticity) - the error variance should be constant

- Independence - the errors associated with one observation are not correlated with the errors of any other observation

- Errors in variables - predictor variables are measured without error (we will cover this in Chapter 4)

- Model specification - the model should be properly specified (including all relevant variables, and excluding irrelevant variables)

Additionally, there are issues that can arise during the analysis that, while strictly speaking, are not assumptions of regression, are none the less, of great concern to regression analysts.

- Influence - individual observations that exert undue influence on the coefficients

- Collinearity - predictors that are highly collinear, i.e. linearly related, can cause problems in estimating the regression coefficients.

2.1 Unusual and influential data

A single observation that is substantially different from all other observations can make a large difference in the results of your regression analysis. If a single observation (or small group of observations) substantially changes your results, you would want to know about this and investigate further. There are three ways that an observation can be unusual.

Outliers: In linear regression, an outlier is an observation with large residual. In other words, it is an observation whose dependent-variable value is unusual given its values on the predictor variables. An outlier may indicate a sample peculiarity or may indicate a data entry error or other problem.

Leverage: An observation with an extreme value on a predictor variable is called a point with high leverage. Leverage is a measure of how far an observation deviates from the mean of that variable. These leverage points can have an effect on the estimate of regression coefficients.

Influence: An observation is said to be influential if removing the observation substantially changes the estimate of coefficients. Influence can be thought of as the product of leverage and outlierness.

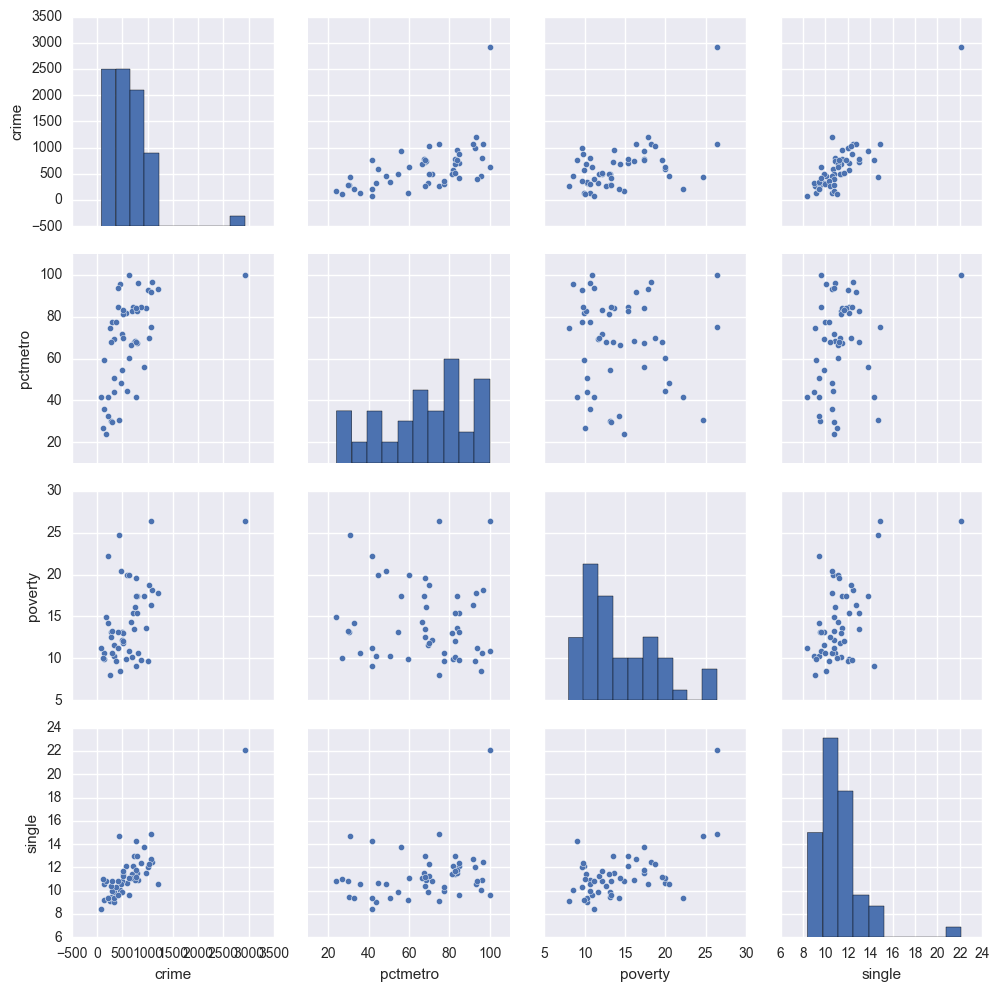

How can we identify these three types of observations? Let's look at an example dataset called crime. This dataset appears in Statistical Methods for Social Sciences, Third Edition by Alan Agresti and Barbara Finlay (Prentice Hall, 1997). The variables are state id (sid), state name (state), violent crimes per 100,000 people (crime), murders per 1,000,000 (murder), the percent of the population living in metropolitan areas (pctmetro), the percent of the population that is white (pctwhite), percent of population with a high school education or above (pcths), percent of population living under poverty line (poverty), and percent of population that are single parents (single).

import pandas as pd

import numpy as np

import itertools

from itertools import chain, combinations

import statsmodels.formula.api as smf

import scipy.stats as scipystats

import statsmodels.api as sm

import statsmodels.stats.stattools as stools

import statsmodels.stats as stats

from statsmodels.graphics.regressionplots import *

import matplotlib.pyplot as plt

import seaborn as sns

import copy

from sklearn.cross_validation import train_test_split

import math

import time

%matplotlib inline

plt.rcParams['figure.figsize'] = (16, 12)

mypath = r'D:\Dropbox\ipynb_download\ipynb_blog\\'

crime = pd.read_csv(mypath + r'crime.csv')

crime.describe()

| sid | crime | murder | pctmetro | pctwhite | pcths | poverty | single | |

|---|---|---|---|---|---|---|---|---|

| count | 51.000000 | 51.000000 | 51.000000 | 51.000000 | 51.000000 | 51.000000 | 51.000000 | 51.000000 |

| mean | 26.000000 | 612.843137 | 8.727451 | 67.390196 | 84.115686 | 76.223529 | 14.258824 | 11.325490 |

| std | 14.866069 | 441.100323 | 10.717576 | 21.957133 | 13.258392 | 5.592087 | 4.584242 | 2.121494 |

| min | 1.000000 | 82.000000 | 1.600000 | 24.000000 | 31.800000 | 64.300000 | 8.000000 | 8.400000 |

| 25% | 13.500000 | 326.500000 | 3.900000 | 49.550000 | 79.350000 | 73.500000 | 10.700000 | 10.050000 |

| 50% | 26.000000 | 515.000000 | 6.800000 | 69.800000 | 87.600000 | 76.700000 | 13.100000 | 10.900000 |

| 75% | 38.500000 | 773.000000 | 10.350000 | 83.950000 | 92.600000 | 80.100000 | 17.400000 | 12.050000 |

| max | 51.000000 | 2922.000000 | 78.500000 | 100.000000 | 98.500000 | 86.600000 | 26.400000 | 22.100000 |

sns.pairplot(crime[['crime', 'pctmetro', 'poverty', 'single']].dropna(how = 'any', axis = 0))

<seaborn.axisgrid.PairGrid at 0x176314a8>

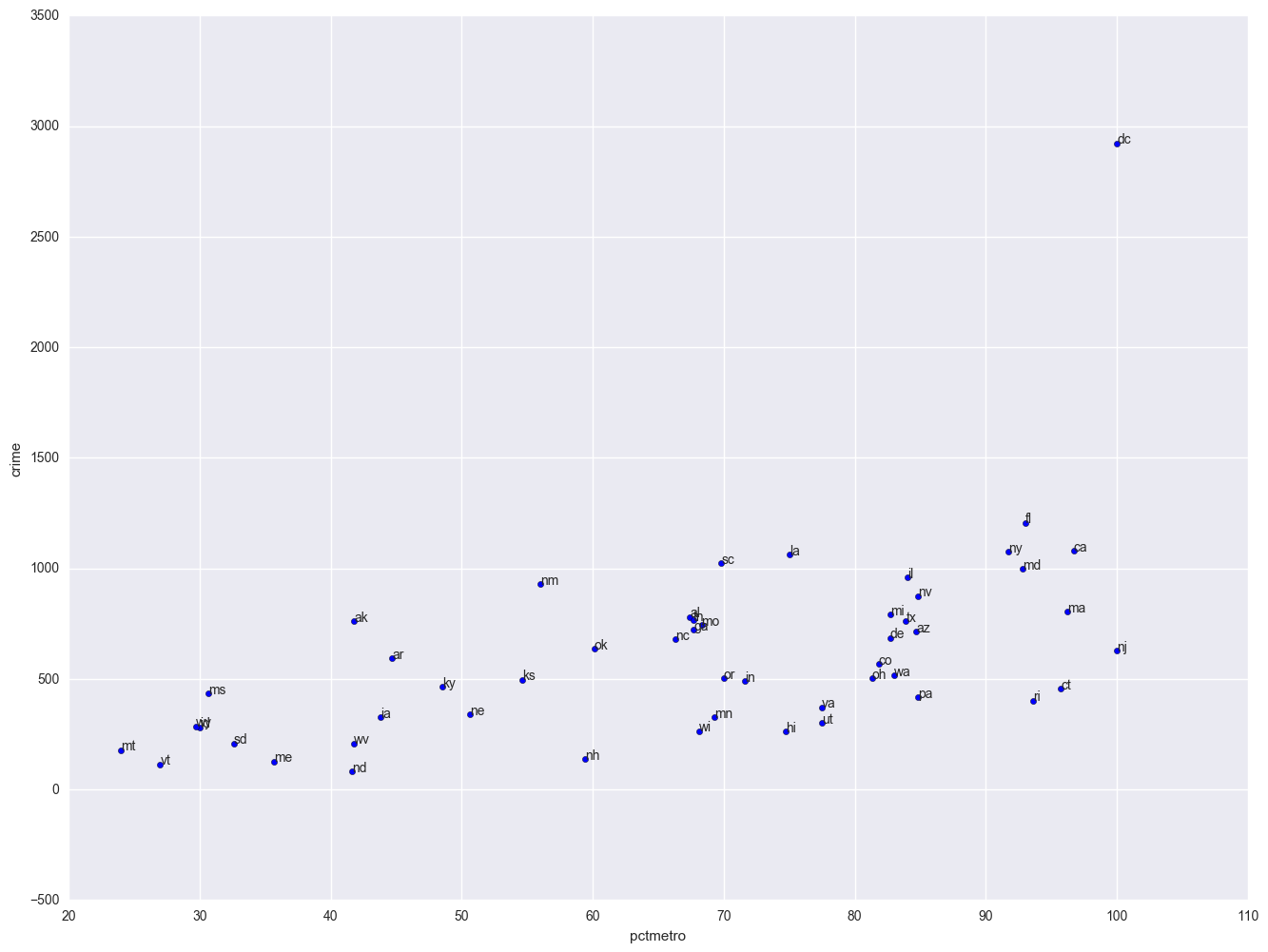

The graphs of crime with other variables show some potential problems. In every plot, we see a data point that is far away from the rest of the data points. Let's make individual graphs of crime with pctmetro and poverty and single so we can get a better view of these scatterplots. We will add the label plot of the state name instead of a point.

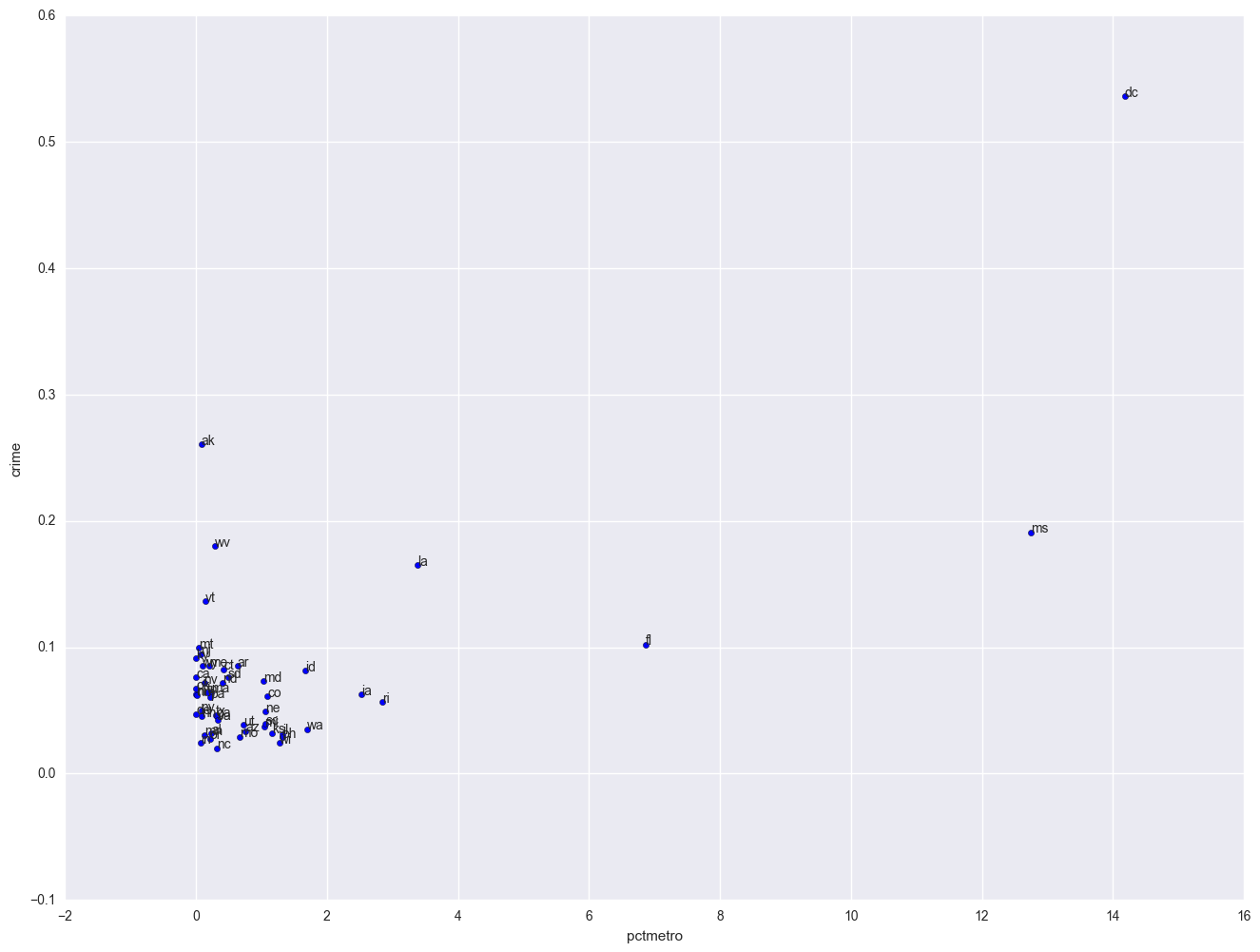

plt.scatter(crime.pctmetro, crime.crime)

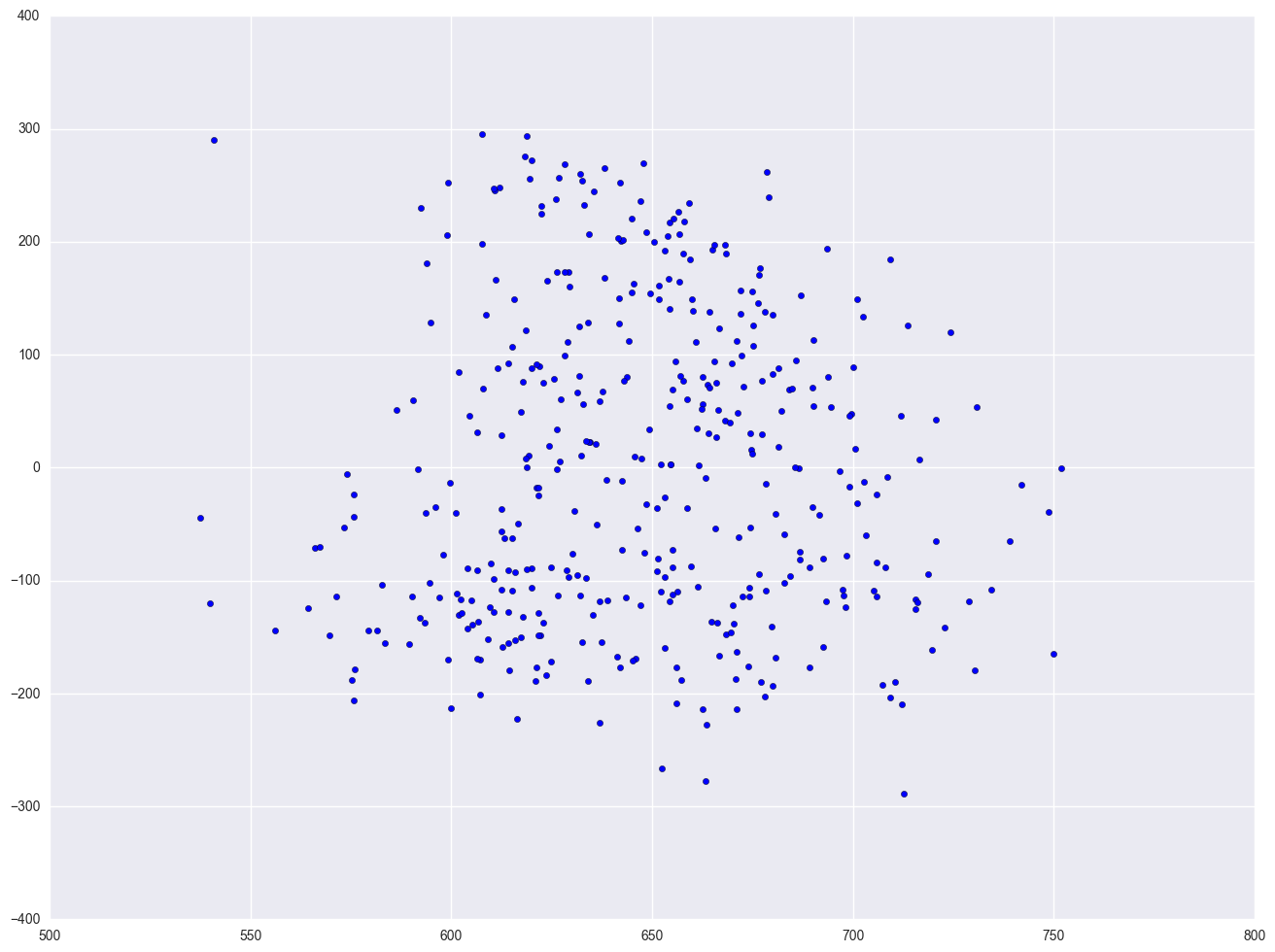

for i, state in enumerate(crime.state):

plt.annotate(state, [crime.pctmetro[i], crime.crime[i]])

plt.xlabel("pctmetro")

plt.ylabel("crime")

<matplotlib.text.Text at 0x130b47f0>

All the scatter plots suggest that the observation for state = dc is a point that requires extra attention since it stands out away from all of the other points. We will keep it in mind when we do our regression analysis.

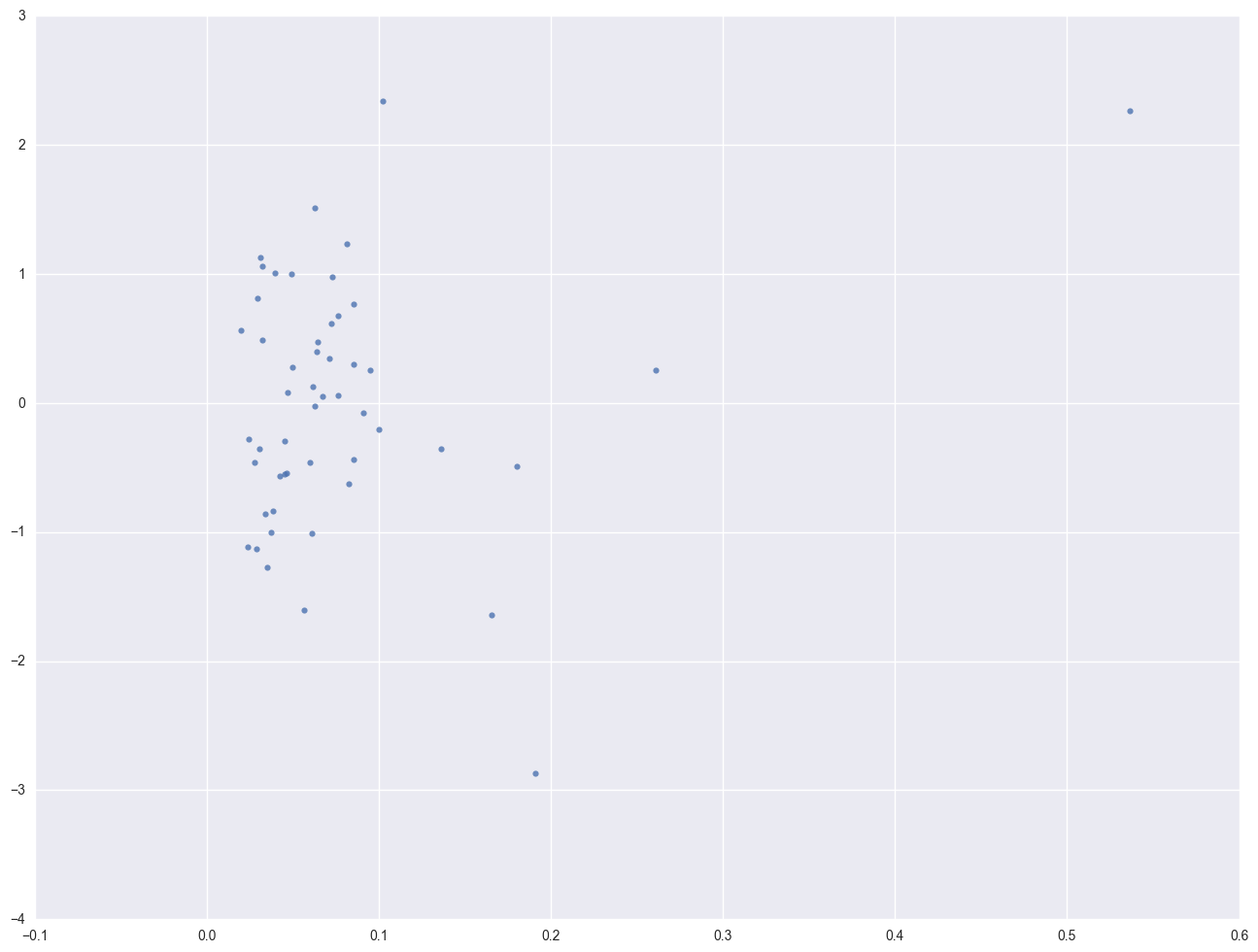

Now let's try the regression predicting crime from pctmetro, poverty and single. We will go step-by-step to identify all the potentially unusual or influential points afterwards. We will output several statistics that we will need for the next few analyses to a dataset called crime1res, and we will explain each statistic in turn. These statistics include the studentized residual (called resid_student), leverage (called leverage), Cook's D (called cooks) and DFFITS (called dffits). We are requesting all of these statistics now so that they can be placed in a single dataset that we will use for the next several examples.

pd.Series(influence.hat_matrix_diag).describe()

count 51.000000

mean 0.078431

std 0.080285

min 0.020061

25% 0.037944

50% 0.061847

75% 0.083896

max 0.536383

dtype: float64

lm = smf.ols(formula = "crime ~ pctmetro + poverty + single", data = crime).fit()

print lm.summary()

influence = lm.get_influence()

resid_student = influence.resid_studentized_external

(cooks, p) = influence.cooks_distance

(dffits, p) = influence.dffits

leverage = influence.hat_matrix_diag

print '\n'

print 'Leverage v.s. Studentized Residuals'

sns.regplot(leverage, lm.resid_pearson, fit_reg=False)

OLS Regression Results

==============================================================================

Dep. Variable: crime R-squared: 0.840

Model: OLS Adj. R-squared: 0.830

Method: Least Squares F-statistic: 82.16

Date: Mon, 26 Dec 2016 Prob (F-statistic): 1.03e-18

Time: 07:12:55 Log-Likelihood: -335.71

No. Observations: 51 AIC: 679.4

Df Residuals: 47 BIC: 687.1

Df Model: 3

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [95.0% Conf. Int.]

------------------------------------------------------------------------------

Intercept -1666.4359 147.852 -11.271 0.000 -1963.876 -1368.996

pctmetro 7.8289 1.255 6.240 0.000 5.305 10.353

poverty 17.6802 6.941 2.547 0.014 3.717 31.644

single 132.4081 15.503 8.541 0.000 101.220 163.597

==============================================================================

Omnibus: 2.081 Durbin-Watson: 1.706

Prob(Omnibus): 0.353 Jarque-Bera (JB): 1.284

Skew: -0.093 Prob(JB): 0.526

Kurtosis: 3.755 Cond. No. 424.

==============================================================================

Warnings:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

Leverage v.s. Studentized Residuals

<matplotlib.axes._subplots.AxesSubplot at 0x1baf2f28>

crime1res = pd.concat([pd.Series(cooks, name = "cooks"), pd.Series(dffits, name = "dffits"), pd.Series(leverage, name = "leverage"), pd.Series(resid_student, name = "resid_student")], axis = 1)

crime1res = pd.concat([crime, crime1res], axis = 1)

crime1res.head()

| sid | state | crime | murder | pctmetro | pctwhite | pcths | poverty | single | cooks | dffits | leverage | resid_student | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 1 | ak | 761 | 9.0 | 41.8 | 75.2 | 86.6 | 9.1 | 14.3 | 0.007565 | 0.172247 | 0.260676 | 0.290081 |

| 1 | 2 | al | 780 | 11.6 | 67.4 | 73.5 | 66.9 | 17.4 | 11.5 | 0.002020 | 0.089166 | 0.032089 | 0.489712 |

| 2 | 3 | ar | 593 | 10.2 | 44.7 | 82.9 | 66.3 | 20.0 | 10.7 | 0.014897 | 0.243153 | 0.085385 | 0.795809 |

| 3 | 4 | az | 715 | 8.6 | 84.7 | 88.6 | 78.7 | 15.4 | 12.1 | 0.006654 | -0.162721 | 0.033806 | -0.869915 |

| 4 | 5 | ca | 1078 | 13.1 | 96.7 | 79.3 | 76.2 | 18.2 | 12.5 | 0.000075 | 0.017079 | 0.076468 | 0.059353 |

Let's examine the studentized residuals as a first means for identifying outliers. We requested the studentized residuals in the above regression in the output statement and named them r. Studentized residuals are a type of standardized residual that can be used to identify outliers. We see three residuals that stick out, -3.57, 2.62 and 3.77.

r = crime1res.resid_student

print '-'*30 + ' studentized residual ' + '-'*30

print r.describe()

print '\n'

r_sort = crime1res.sort_values(by = 'resid_student')

print '-'*30 + ' top 5 most negative residuals ' + '-'*30

print r_sort.head()

print '\n'

print '-'*30 + ' top 5 most positive residuals ' + '-'*30

print r_sort.tail()

------------------------------ studentized residual ------------------------------

count 51.000000

mean 0.018402

std 1.133126

min -3.570789

25% -0.555460

50% 0.052616

75% 0.599771

max 3.765847

Name: resid_student, dtype: float64

------------------------------ top 5 most negative residuals ------------------------------

sid state crime murder pctmetro pctwhite pcths poverty single \

24 25 ms 434 13.5 30.7 63.3 64.3 24.7 14.7

17 18 la 1062 20.3 75.0 66.7 68.3 26.4 14.9

38 39 ri 402 3.9 93.6 92.6 72.0 11.2 10.8

46 47 wa 515 5.2 83.0 89.4 83.8 12.1 11.7

34 35 oh 504 6.0 81.3 87.5 75.7 13.0 11.4

cooks dffits leverage resid_student

24 0.602106 -1.735096 0.191012 -3.570789

17 0.159264 -0.818120 0.165277 -1.838578

38 0.041165 -0.413655 0.056803 -1.685598

46 0.015271 -0.248989 0.035181 -1.303919

34 0.009695 -0.197588 0.028755 -1.148330

------------------------------ top 5 most positive residuals ------------------------------

sid state crime murder pctmetro pctwhite pcths poverty single \

13 14 il 960 11.4 84.0 81.0 76.2 13.6 11.5

12 13 id 282 2.9 30.0 96.7 79.7 13.1 9.5

11 12 ia 326 2.3 43.8 96.6 80.1 10.3 9.0

8 9 fl 1206 8.9 93.0 83.5 74.4 17.8 10.6

50 51 dc 2922 78.5 100.0 31.8 73.1 26.4 22.1

cooks dffits leverage resid_student

13 0.010661 0.207220 0.031358 1.151702

12 0.036675 0.385749 0.081675 1.293477

11 0.040978 0.411382 0.062768 1.589644

8 0.173629 0.883820 0.102202 2.619523

50 3.203429 4.050610 0.536383 3.765847

We should pay attention to studentized residuals that exceed +2 or -2, and get even more concerned about residuals that exceed +2.5 or -2.5 and even yet more concerned about residuals that exceed +3 or -3. These results show that DC and MS are the most worrisome observations, followed by FL.

Let's show all of the variables in our regression where the studentized residual exceeds +2 or -2, i.e., where the absolute value of the residual exceeds 2. We see the data for the three potential outliers we identified, namely Florida, Mississippi and Washington D.C. Looking carefully at these three observations, we couldn't find any data entry errors, though we may want to do another regression analysis with the extreme point such as DC deleted. We will return to this issue later.

print crime[abs(r) > 2]

sid state crime murder pctmetro pctwhite pcths poverty single

8 9 fl 1206 8.9 93.0 83.5 74.4 17.8 10.6

24 25 ms 434 13.5 30.7 63.3 64.3 24.7 14.7

50 51 dc 2922 78.5 100.0 31.8 73.1 26.4 22.1

Now let's look at the leverage's to identify observations that will have potential great influence on regression coefficient estimates.

Generally, a point with leverage greater than (2k+2)/n should be carefully examined, where k is the number of predictors and n is the number of observations. In our example this works out to (2*3+2)/51 = .15686275, so we can do the following.

leverage = crime1res.leverage

print '-'*30 + ' Leverage ' + '-'*30

print leverage.describe()

print '\n'

leverage_sort = crime1res.sort_values(by = 'leverage', ascending = False)

print '-'*30 + ' top 5 highest leverage data points ' + '-'*30

print leverage_sort.head()

------------------------------ Leverage ------------------------------

count 51.000000

mean 0.078431

std 0.080285

min 0.020061

25% 0.037944

50% 0.061847

75% 0.083896

max 0.536383

Name: leverage, dtype: float64

------------------------------ top 5 highest leverage data points ------------------------------

sid state crime murder pctmetro pctwhite pcths poverty single \

50 51 dc 2922 78.5 100.0 31.8 73.1 26.4 22.1

0 1 ak 761 9.0 41.8 75.2 86.6 9.1 14.3

24 25 ms 434 13.5 30.7 63.3 64.3 24.7 14.7

48 49 wv 208 6.9 41.8 96.3 66.0 22.2 9.4

17 18 la 1062 20.3 75.0 66.7 68.3 26.4 14.9

cooks dffits leverage resid_student

50 3.203429 4.050610 0.536383 3.765847

0 0.007565 0.172247 0.260676 0.290081

24 0.602106 -1.735096 0.191012 -3.570789

48 0.016361 -0.253893 0.180200 -0.541535

17 0.159264 -0.818120 0.165277 -1.838578

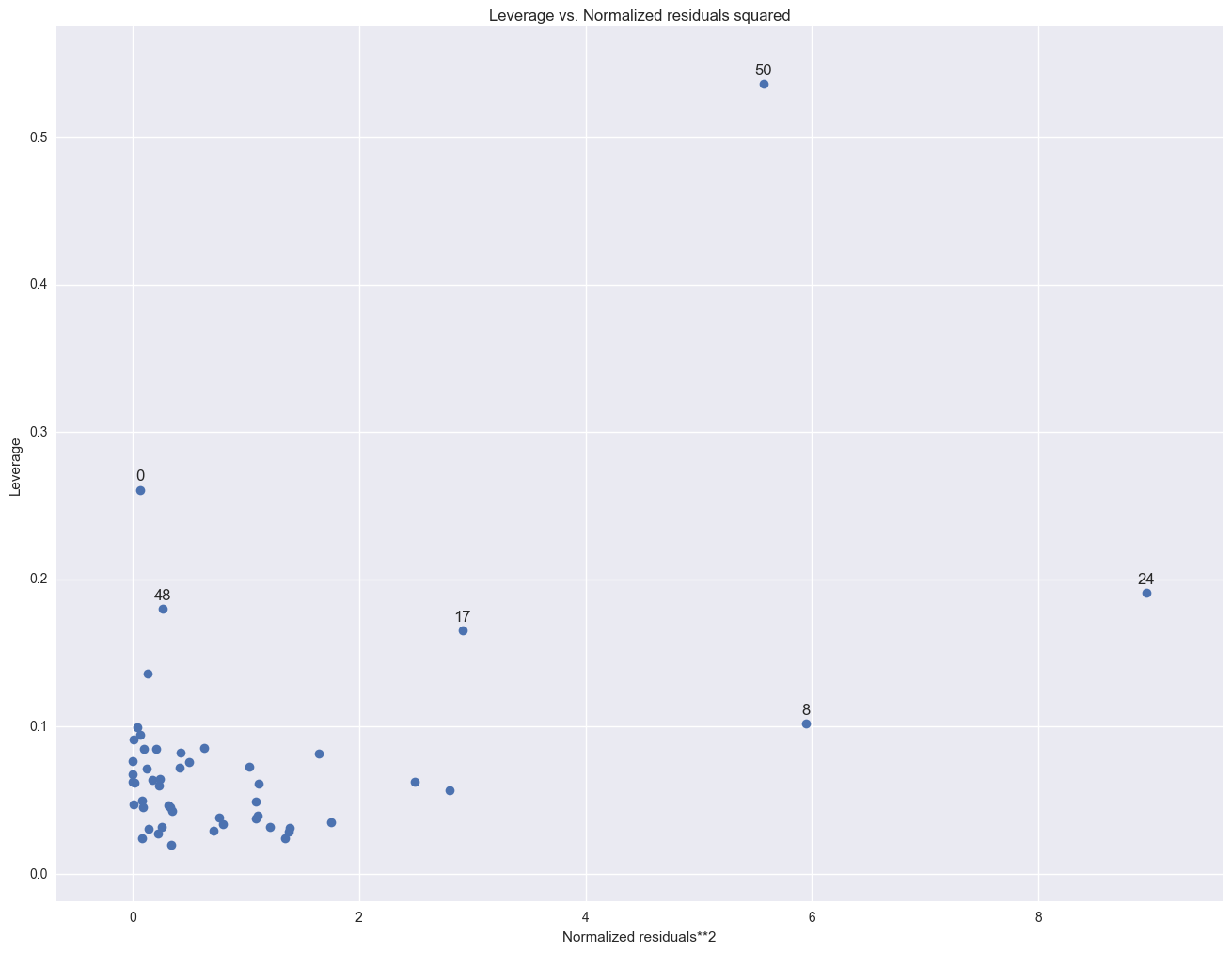

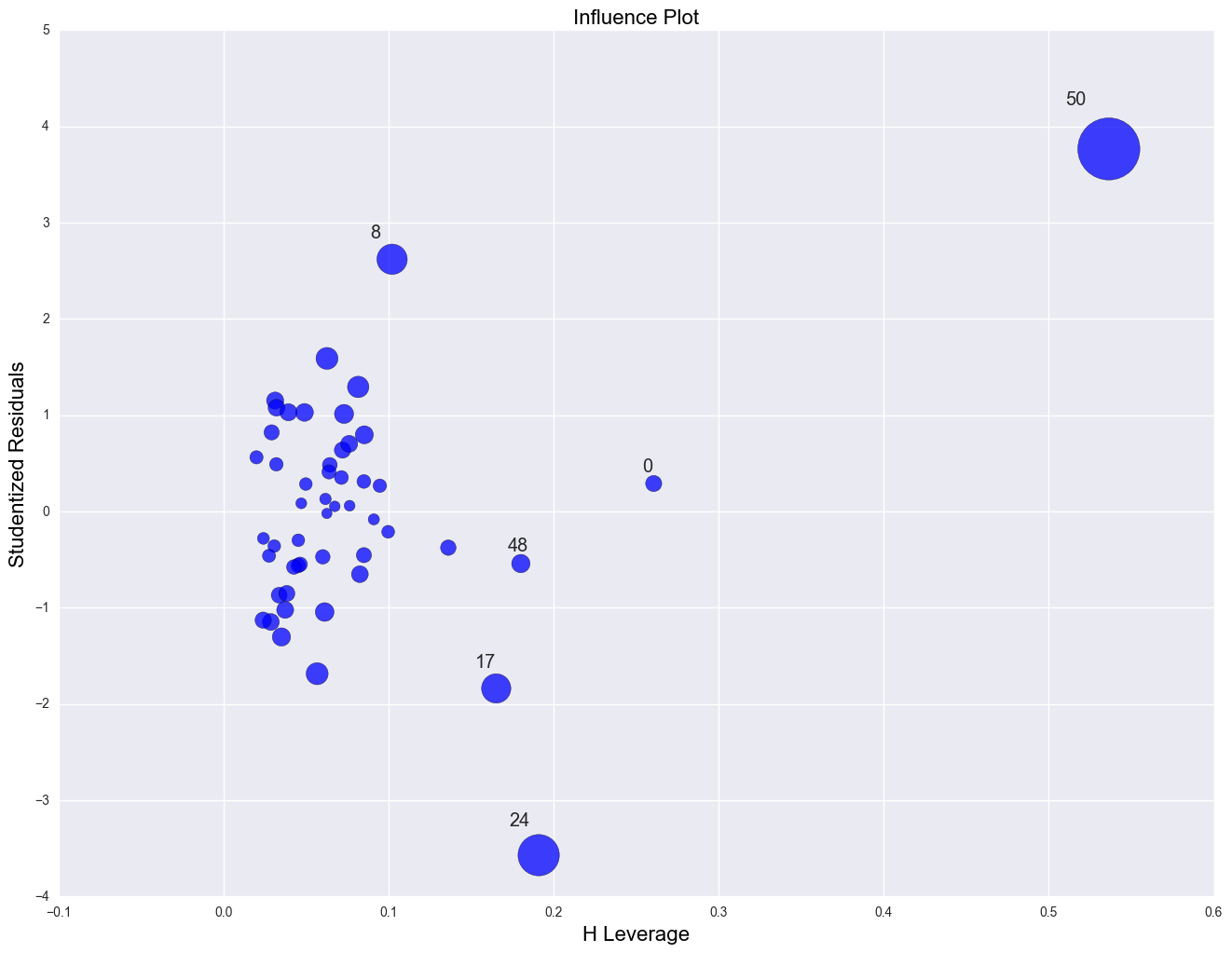

As we have seen, DC is an observation that both has a large residual and large leverage. Such points are potentially the most influential. We can make a plot that shows the leverage by the residual squared and look for observations that are jointly high on both of these measures. We can do this using a leverage versus residual-squared plot. Using residual squared instead of residual itself, the graph is restricted to the first quadrant and the relative positions of data points are preserved. This is a quick way of checking potential influential observations and outliers at the same time. Both types of points are of great concern for us.

from statsmodels.graphics.regressionplots import *

plot_leverage_resid2(lm)

plt.show()

plt.scatter(crime1res.resid_student ** 2, crime1res.leverage)

for i, state in enumerate(crime.state):

plt.annotate(state, [(crime1res.resid_student ** 2)[i], crime1res.leverage[i]])

plt.xlabel("pctmetro")

plt.ylabel("crime")

plt.show()

influence_plot(lm)

plt.show()

The point for DC catches our attention having both the highest residual squared and highest leverage, suggesting it could be very influential. The point for MS has almost as large a residual squared, but does not have the same leverage. We'll look at those observations more carefully by listing them below.

Now let's move on to overall measures of influence. Specifically, let's look at Cook's D and DFITS. These measures both combine information on the residual and leverage. Cook's D and DFITS are very similar except that they scale differently, but they give us similar answers.

The lowest value that Cook's D can assume is zero, and the higher the Cook's D is, the more influential the point is. The conventional cut-off point is 4/n. We can list any observation above the cut-off point by doing the following. We do see that the Cook's D for DC is by far the largest.

Now let's take a look at DFITS. The conventional cut-off point for DFITS is 2*sqrt(k/n). DFITS can be either positive or negative, with numbers close to zero corresponding to the points with small or zero influence. As we see, DFITS also indicates that DC is, by far, the most influential observation.

crime1res[abs(crime1res.dffits) > 2 * math.sqrt(3.0 / 51)]

| sid | state | crime | murder | pctmetro | pctwhite | pcths | poverty | single | cooks | dffits | leverage | resid_student | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 8 | 9 | fl | 1206 | 8.9 | 93.0 | 83.5 | 74.4 | 17.8 | 10.6 | 0.173629 | 0.883820 | 0.102202 | 2.619523 |

| 17 | 18 | la | 1062 | 20.3 | 75.0 | 66.7 | 68.3 | 26.4 | 14.9 | 0.159264 | -0.818120 | 0.165277 | -1.838578 |

| 24 | 25 | ms | 434 | 13.5 | 30.7 | 63.3 | 64.3 | 24.7 | 14.7 | 0.602106 | -1.735096 | 0.191012 | -3.570789 |

| 50 | 51 | dc | 2922 | 78.5 | 100.0 | 31.8 | 73.1 | 26.4 | 22.1 | 3.203429 | 4.050610 | 0.536383 | 3.765847 |

The above measures are general measures of influence. You can also consider more specific measures of influence that assess how each coefficient is changed by deleting the observation. This measure is called DFBETA and is created for each of the predictors. Apparently this is more computationally intensive than summary statistics such as Cook's D because the more predictors a model has, the more computation it may involve. We can restrict our attention to only those predictors that we are most concerned with and to see how well behaved those predictors are.

crimedfbeta = pd.concat([crime1res, pd.DataFrame(influence.dfbetas, columns = ['dfb_intercept', 'dfb_pctmetro', 'dfb_poverty', 'dfb_single'])], axis = 1)

print crimedfbeta.head()

# print pd.DataFrame(OLSInfluence(lm).dfbetas).head()

sid state crime murder pctmetro pctwhite pcths poverty single \

0 1 ak 761 9.0 41.8 75.2 86.6 9.1 14.3

1 2 al 780 11.6 67.4 73.5 66.9 17.4 11.5

2 3 ar 593 10.2 44.7 82.9 66.3 20.0 10.7

3 4 az 715 8.6 84.7 88.6 78.7 15.4 12.1

4 5 ca 1078 13.1 96.7 79.3 76.2 18.2 12.5

cooks dffits leverage resid_student dfb_intercept dfb_pctmetro \

0 0.007565 0.172247 0.260676 0.290081 -0.015624 -0.106185

1 0.002020 0.089166 0.032089 0.489712 0.000577 0.012429

2 0.014897 0.243153 0.085385 0.795809 0.067038 -0.068748

3 0.006654 -0.162721 0.033806 -0.869915 0.052022 -0.094761

4 0.000075 0.017079 0.076468 0.059353 -0.007311 0.012640

dfb_poverty dfb_single

0 -0.131340 0.145183

1 0.055285 -0.027513

2 0.175348 -0.105263

3 -0.030883 0.001242

4 0.008801 -0.003636

The value for DFB_single for Alaska is 0.14, which means that by being included in the analysis (as compared to being excluded), Alaska increases the coefficient for single by 0.14 standard errors, i.e., 0.14 times the standard error for BSingle or by (0.14 * 15.5). Because the inclusion of an observation could either contribute to an increase or decrease in a regression coefficient, DFBETAs can be either positive or negative. A DFBETA value in excess of 2/sqrt(n) merits further investigation. In this example, we would be concerned about absolute values in excess of 2/sqrt(51) or 0.28.

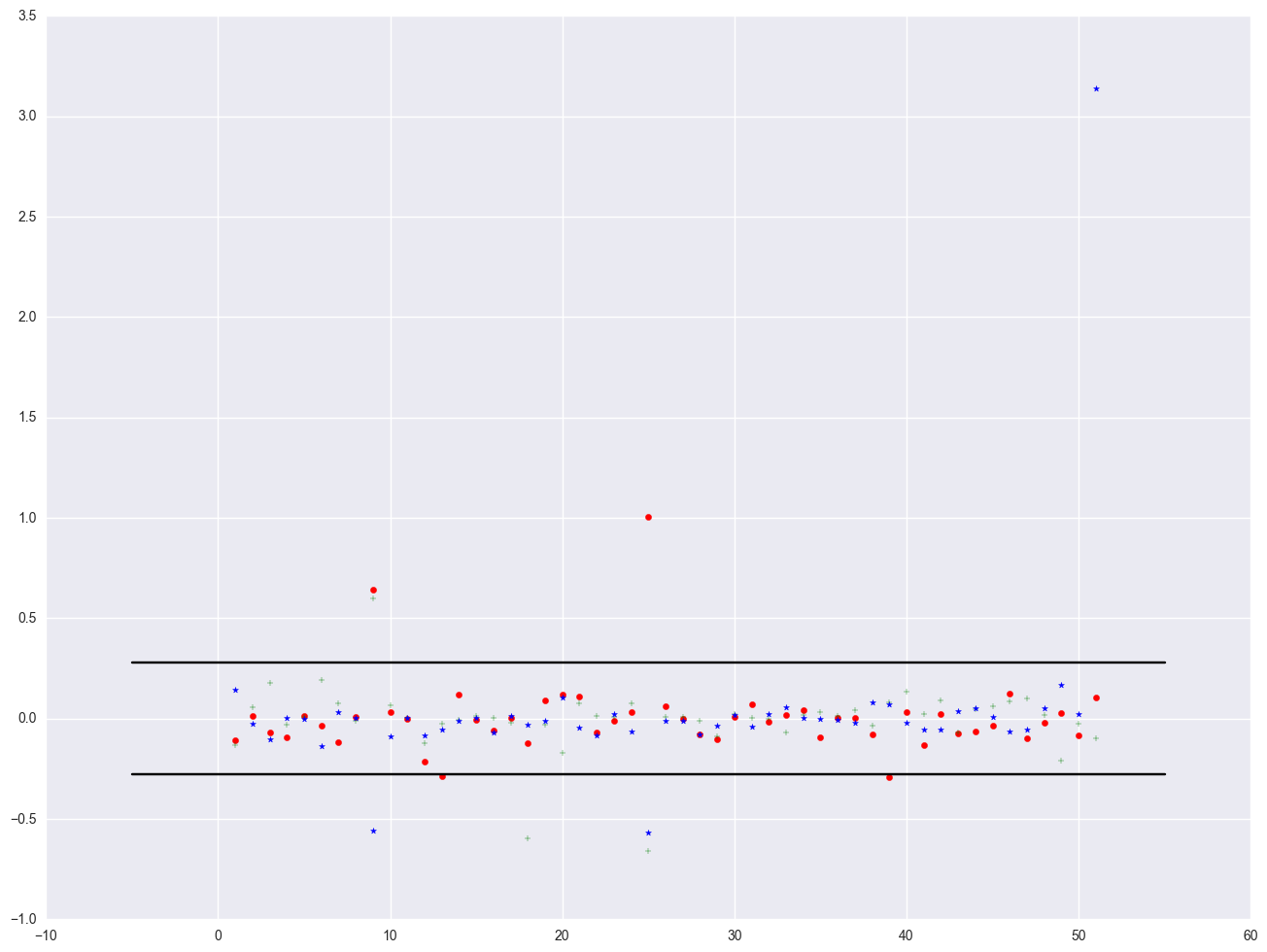

We can plot all three DFBETA values against the state id in one graph shown below. We add a line at 0.28 and -0.28 to help us see potentially troublesome observations. We see the largest value is about 3.0 for DFsingle.

plt.scatter(crimedfbeta.sid, crimedfbeta.dfb_pctmetro, color = "red", marker = "o")

plt.scatter(crimedfbeta.sid, crimedfbeta.dfb_poverty, color = "green", marker = "+")

plt.scatter(crimedfbeta.sid, crimedfbeta.dfb_single, color = "blue", marker = "*")

# add a horizontial line in pyplot, using plt.plot((x1, x2), (y1, y2), 'c-')

plt.plot((-5, 55), (0.28, 0.28), 'k-')

plt.plot((-5, 55), (-0.28, -0.28), 'k-')

[<matplotlib.lines.Line2D at 0x23161ac8>]

Finally, all the analysis showing data point with 'dc' is the most problematic observation. Let's run the regression without the 'dc' point.

lm_1 = smf.ols(formula = "crime ~ pctmetro + poverty + single", data = crime[crime.state != "dc"]).fit()

print lm_1.summary()

OLS Regression Results

==============================================================================

Dep. Variable: crime R-squared: 0.722

Model: OLS Adj. R-squared: 0.704

Method: Least Squares F-statistic: 39.90

Date: Mon, 26 Dec 2016 Prob (F-statistic): 7.45e-13

Time: 07:48:06 Log-Likelihood: -322.90

No. Observations: 50 AIC: 653.8

Df Residuals: 46 BIC: 661.5

Df Model: 3

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [95.0% Conf. Int.]

------------------------------------------------------------------------------

Intercept -1197.5381 180.487 -6.635 0.000 -1560.840 -834.236

pctmetro 7.7123 1.109 6.953 0.000 5.480 9.945

poverty 18.2827 6.136 2.980 0.005 5.932 30.634

single 89.4008 17.836 5.012 0.000 53.498 125.303

==============================================================================

Omnibus: 0.112 Durbin-Watson: 1.760

Prob(Omnibus): 0.945 Jarque-Bera (JB): 0.144

Skew: 0.098 Prob(JB): 0.930

Kurtosis: 2.825 Cond. No. 574.

==============================================================================

Warnings:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

Summary

In this section, we explored a number of methods of identifying outliers and influential points. In a typical analysis, you would probably use only some of these methods. Generally speaking, there are two types of methods for assessing outliers: statistics such as residuals, leverage, Cook's D and DFITS, that assess the overall impact of an observation on the regression results, and statistics such as DFBETA that assess the specific impact of an observation on the regression coefficients.

In our example, we found that DC was a point of major concern. We performed a regression with it and without it and the regression equations were very different. We can justify removing it from our analysis by reasoning that our model is to predict crime rate for states, not for metropolitan areas.

2.2 Tests for Normality of Residuals

One of the assumptions of linear regression analysis is that the residuals are normally distributed. This assumption assures that the p-values for the t-tests will be valid. As before, we will generate the residuals (called r) and predicted values (called fv) and put them in a dataset (called elem1res). We will also keep the variables api00, meals, ell and emer in that dataset.

Let's use the elemapi2 data file we saw in Chapter 1 for these analyses. Let's predict academic performance (api00) from percent receiving free meals (meals), percent of English language learners (ell), and percent of teachers with emergency credentials (emer).

elemapi2 = pd.read_csv(mypath + 'elemapi2.csv')

lm = smf.ols(formula = "api00 ~ meals + ell + emer", data = elemapi2).fit()

print lm.summary()

elem1res = pd.concat([elemapi2, pd.Series(lm.resid, name = 'resid'), pd.Series(lm.predict(), name = "predict")], axis = 1)

OLS Regression Results

==============================================================================

Dep. Variable: api00 R-squared: 0.836

Model: OLS Adj. R-squared: 0.835

Method: Least Squares F-statistic: 673.0

Date: Mon, 26 Dec 2016 Prob (F-statistic): 4.89e-155

Time: 09:42:41 Log-Likelihood: -2188.5

No. Observations: 400 AIC: 4385.

Df Residuals: 396 BIC: 4401.

Df Model: 3

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [95.0% Conf. Int.]

------------------------------------------------------------------------------

Intercept 886.7033 6.260 141.651 0.000 874.397 899.010

meals -3.1592 0.150 -21.098 0.000 -3.454 -2.865

ell -0.9099 0.185 -4.928 0.000 -1.273 -0.547

emer -1.5735 0.293 -5.368 0.000 -2.150 -0.997

==============================================================================

Omnibus: 2.394 Durbin-Watson: 1.437

Prob(Omnibus): 0.302 Jarque-Bera (JB): 2.168

Skew: 0.170 Prob(JB): 0.338

Kurtosis: 3.119 Cond. No. 171.

==============================================================================

Warnings:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

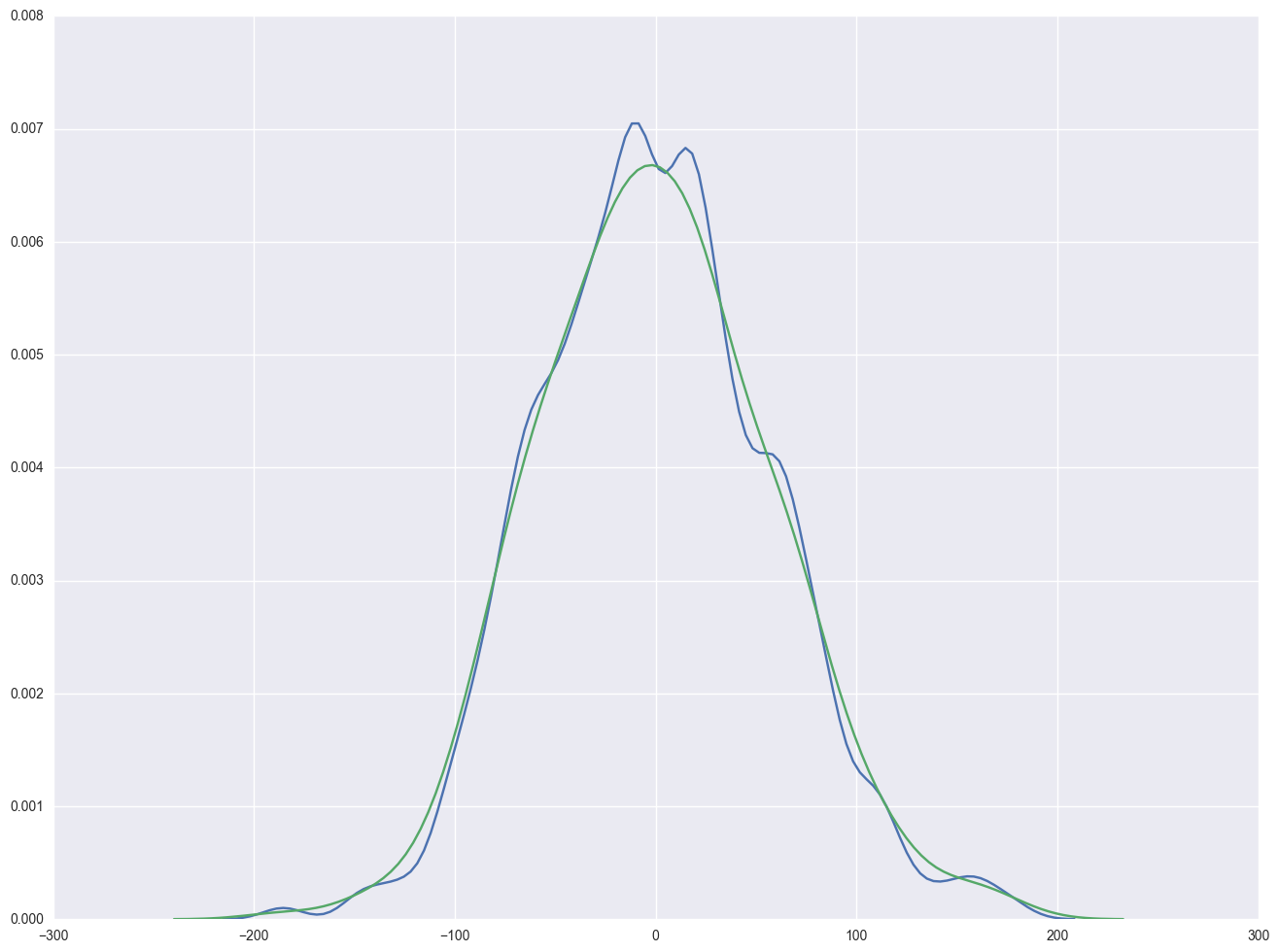

sns.kdeplot(np.array(elem1res.resid), bw=10)

sns.distplot(np.array(elem1res.resid), hist=False)

<matplotlib.axes._subplots.AxesSubplot at 0x23bc05c0>

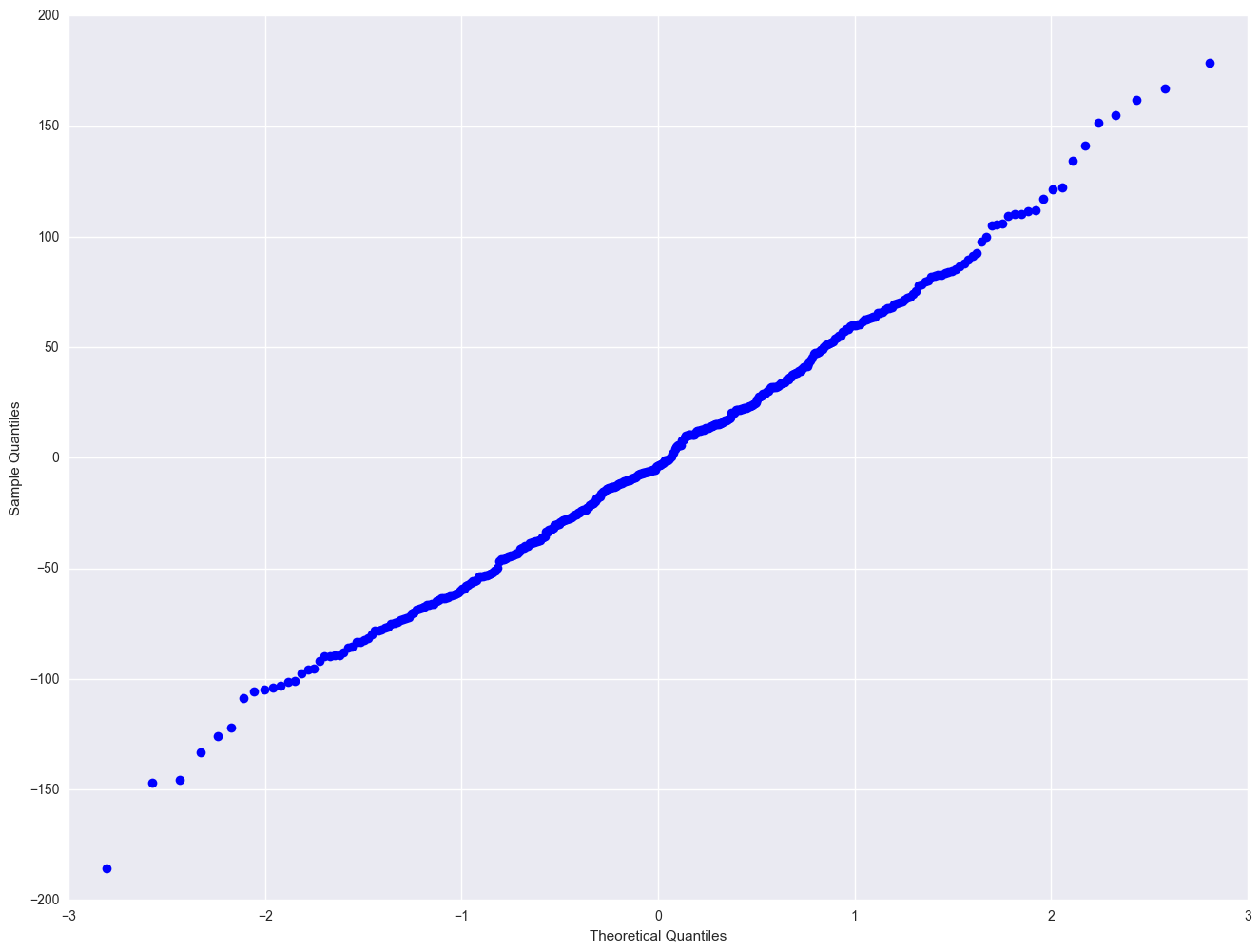

sm.qqplot(elem1res.resid)

plt.show()

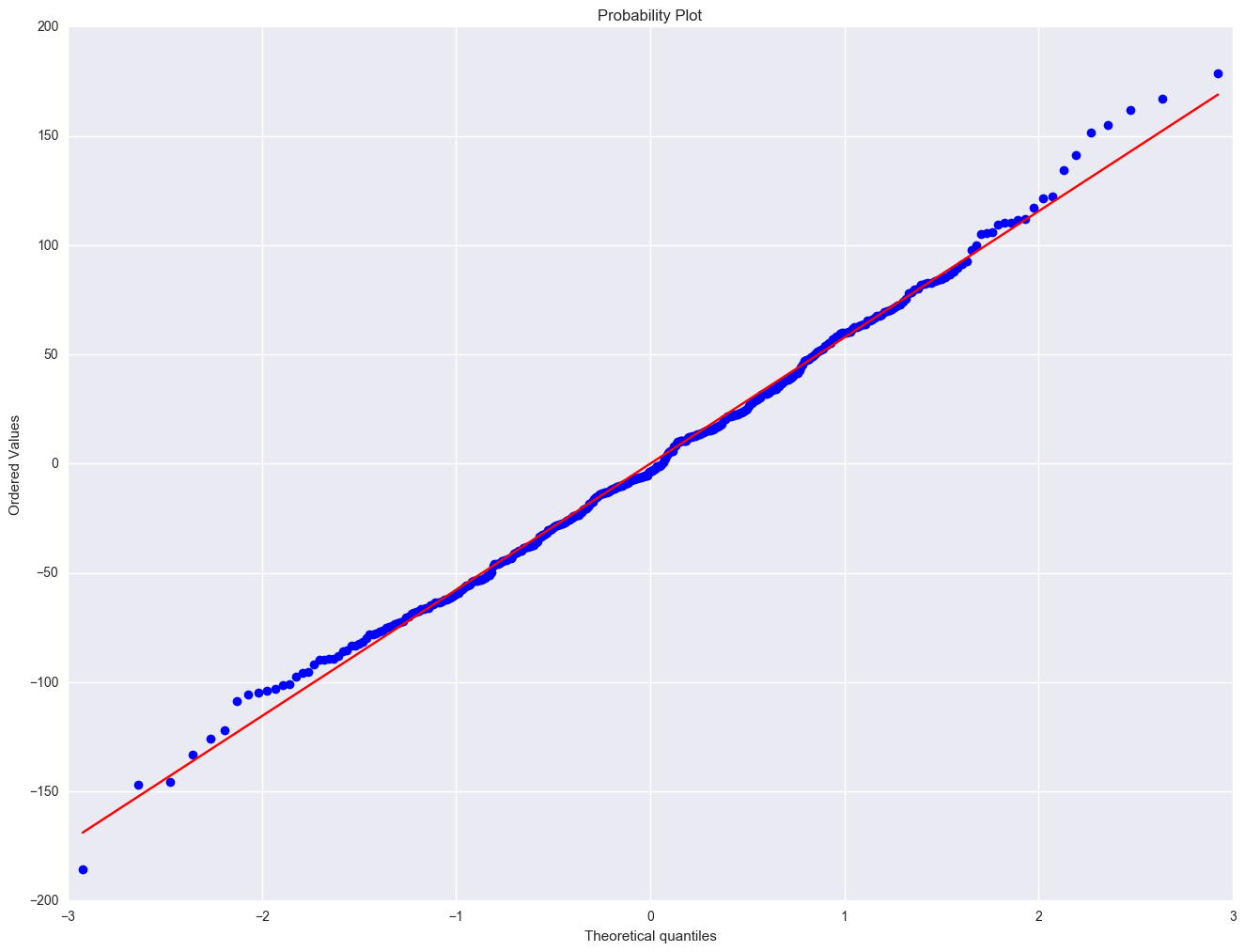

import pylab

scipystats.probplot(elem1res.resid, dist="norm", plot=pylab)

pylab.show()

'''

by default, scipy stats.kstest for normal will assume mean 0 and stdev 1. To use this, the data should be normalized first

'''

resid = elem1res.resid

norm_resid = (elem1res.resid - np.mean(elem1res.resid)) / np.std(elem1res.resid)

print scipystats.kstest(norm_resid, 'norm')

# or use the statsmodels provided function kstest_normal to use kolmogorov-smirnov test or Anderson-Darling test

print stats.diagnostic.kstest_normal(elem1res.resid, pvalmethod='approx')

print stats.diagnostic.normal_ad(elem1res.resid)

KstestResult(statistic=0.032723261818185578, pvalue=0.78506446901572213)

(0.032676218847940308, 0.35190400492542645)

(0.34071240334691311, 0.49471893268937844)

Severe outliers consist of those points that are either 3 inter-quartile-ranges below the first quartile or 3 inter-quartile-ranges above the third quartile. The presence of any severe outliers should be sufficient evidence to reject normality at a 5% significance level. Mild outliers are common in samples of any size. In our case, we don't have any severe outliers and the distribution seems fairly symmetric. The residuals have an approximately normal distribution. (See the output of the proc univariate above.)

In the Kilmogorov-Smirnov test or Anderson-Darling test for normality, the p-value is based on the assumption that the distribution is normal. In our example, the p-value is very large, indicating that we cannot reject that residuals is normally distributed.

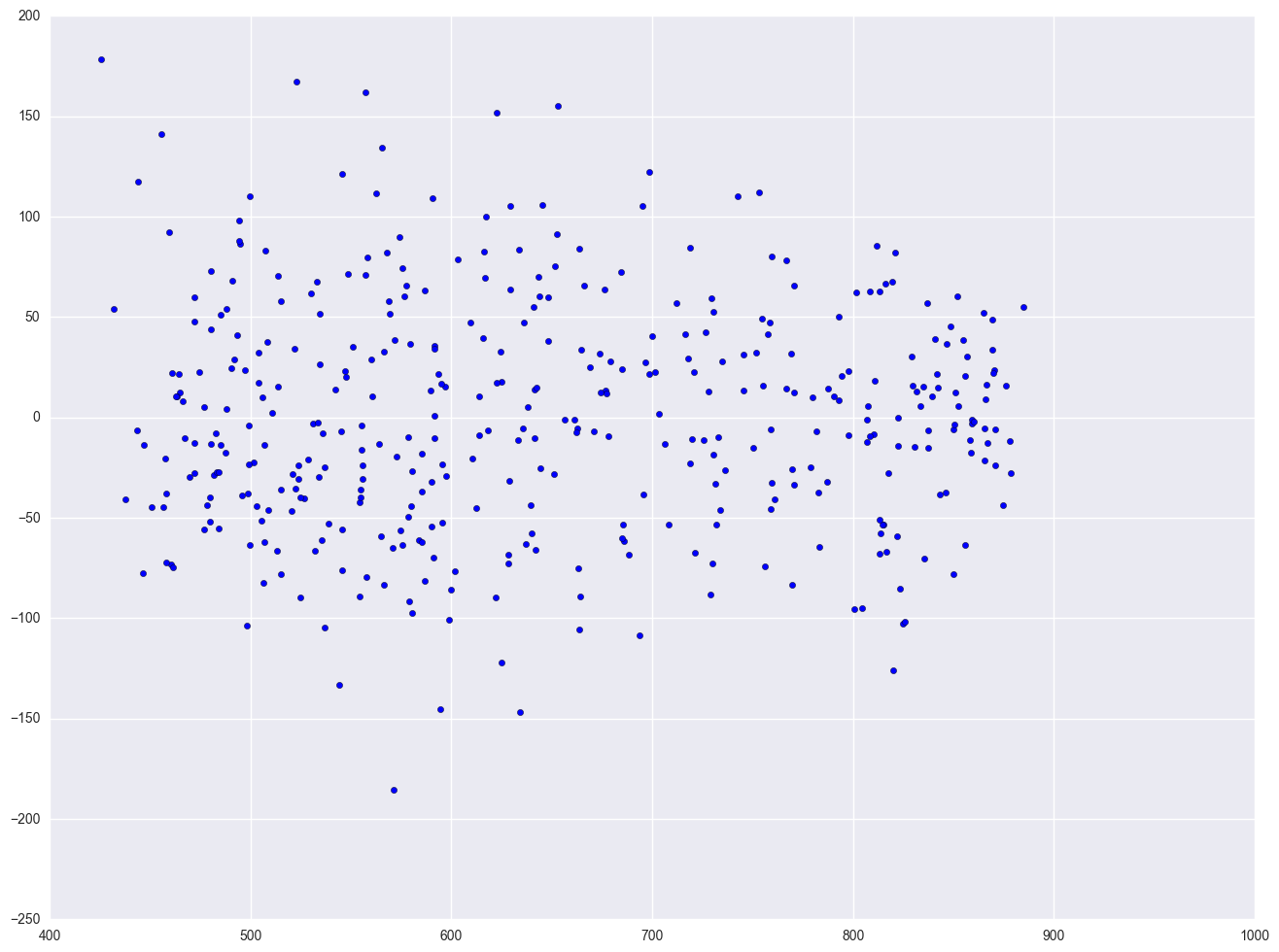

2.3 Tests for Heteroscedasticity

One of the main assumptions for the ordinary least squares regression is the homogeneity of variance of the residuals. If the model is well-fitted, there should be no pattern to the residuals plotted against the fitted values. If the variance of the residuals is non-constant, then the residual variance is said to be "heteroscedastic." There are graphical and non-graphical methods for detecting heteroscedasticity. A commonly used graphical method is to plot the residuals versus fitted (predicted) values. We see that the pattern of the data points is getting a little narrower towards the right end, which is an indication of mild heteroscedasticity.

lm = smf.ols(formula = "api00 ~ meals + ell + emer", data = elemapi2).fit()

resid = lm.resid

plt.scatter(lm.predict(), resid)

<matplotlib.collections.PathCollection at 0x261445f8>

# p-value here is different from SAS output, need double check

stats.diagnostic.het_white(resid, lm.model.exog, retres = False)

(18.352755736667305,

0.031294634010796941,

2.0838250344433504,

0.029987789753355969)

lm2 = smf.ols(formula = "api00 ~ enroll", data = elemapi2).fit()

plt.scatter(lm2.predict(), lm2.resid)

<matplotlib.collections.PathCollection at 0x25ccb470>

elemapi2['log_enroll'] = elemapi2.enroll.map(lambda x: math.log(x))

lm3 = smf.ols(formula = "api00 ~ log_enroll", data = elemapi2).fit()

plt.scatter(lm3.predict(), lm3.resid)

<matplotlib.collections.PathCollection at 0x28a10a20>

Finally, let's revisit the model we used at the start of this section, predicting api00 from meals, ell and emer. Using this model, the distribution of the residuals looked very nice and even across the fitted values. What if we add enroll to this model? Will this automatically ruin the distribution of the residuals? Let's add it and see.

lm4 = smf.ols(formula = "api00 ~ meals + ell + emer + enroll", data = elemapi2).fit()

resid = lm4.resid

plt.scatter(lm4.predict(), resid)

<matplotlib.collections.PathCollection at 0x28b71828>

As you can see, the distribution of the residuals looks fine, even after we added the variable enroll. When we had just the variable enroll in the model, we did a log transformation to improve the distribution of the residuals, but when enroll was part of a model with other variables, the residuals looked good enough so that no transformation was needed. This illustrates how the distribution of the residuals, not the distribution of the predictor, was the guiding factor in determining whether a transformation was needed.

2.4 Tests for Collinearity

When there is a perfect linear relationship among the predictors, the estimates for a regression model cannot be uniquely computed. The term collinearity describes two variables are near perfect linear combinations of one another. When more than two variables are involved, it is often called multicollinearity, although the two terms are often used interchangeably.

The primary concern is that as the degree of multicollinearity increases, the regression model estimates of the coefficients become unstable and the standard errors for the coefficients can get wildly inflated. In this section, we will explore some SAS options used with the model statement that help to detect multicollinearity.

We can use the vif option to check for multicollinearity. vif stands for variance inflation factor. As a rule of thumb, a variable whose VIF values is greater than 10 may merit further investigation. Tolerance, defined as 1/VIF, is used by many researchers to check on the degree of collinearity. A tolerance value lower than 0.1 is comparable to a VIF of 10. It means that the variable could be considered as a linear combination of other independent variables. The tol option on the model statement gives us these values. Let's first look at the regression we did from the last section, the regression model predicting api00 from meals, ell and emer, and use the vif and tol options with the model statement.

from patsy import dmatrices

from statsmodels.stats.outliers_influence import variance_inflation_factor

lm = smf.ols(formula = "api00 ~ meals + ell + emer", data = elemapi2).fit()

y, X = dmatrices("api00 ~ meals + ell + emer", data = elemapi2, return_type = "dataframe")

vif = [variance_inflation_factor(X.values, i) for i in range(X.shape[1])]

print vif

[4.6883371380582997, 2.7250555232887432, 2.5105120172587836, 1.4148169984086651]

We know the multicollinearity is caused the high correlation between the indepentent variables. So let's check the correlation between the vatiables. First we need to drop the added constant column which are all equal to 1. Then np.corrcoef or df.corr will calculate the correlation coefficient. We can also calculate the eigen value and eigen vectors of the correlation matrix to check the details.

corr = np.corrcoef(X.drop("Intercept", axis = 1), rowvar = 0)

print "correlation from np.corrcoef is "

print corr

print '\n'

print "correlation from df.corr() is "

print X.drop("Intercept", axis = 1).corr()

print '\n'

w, v = np.linalg.eig(corr)

print "the eigen value of the correlation coefficient is "

print w

correlation from np.corrcoef is

[[ 1. 0.77237718 0.53303874]

[ 0.77237718 1. 0.47217948]

[ 0.53303874 0.47217948 1. ]]

correlation from df.corr() is

meals ell emer

meals 1.000000 0.772377 0.533039

ell 0.772377 1.000000 0.472179

emer 0.533039 0.472179 1.000000

the eigen value of the correlation coefficient is

[ 2.19536815 0.22351013 0.58112172]

2.5 Tests on Nonlinearity

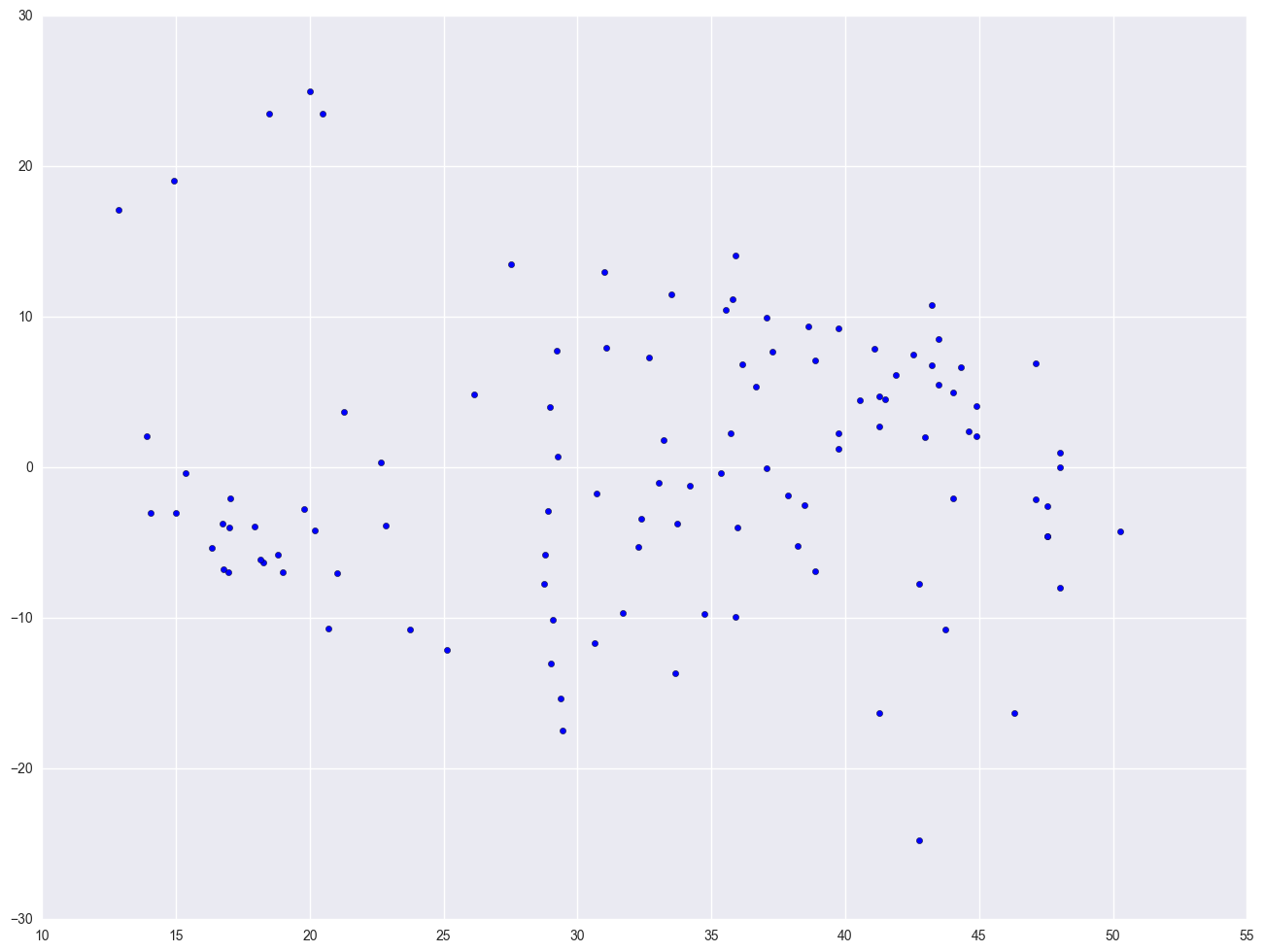

When we do linear regression, we assume that the relationship between the response variable and the predictors is linear. This is the assumption of linearity. If this assumption is violated, the linear regression will try to fit a straight line to data that does not follow a straight line. Checking the linear assumption in the case of simple regression is straightforward, since we only have one predictor. All we have to do is a scatter plot between the response variable and the predictor to see if nonlinearity is present, such as a curved band or a big wave-shaped curve. For example, let us use a data file called nations.sav that has data about a number of nations around the world.

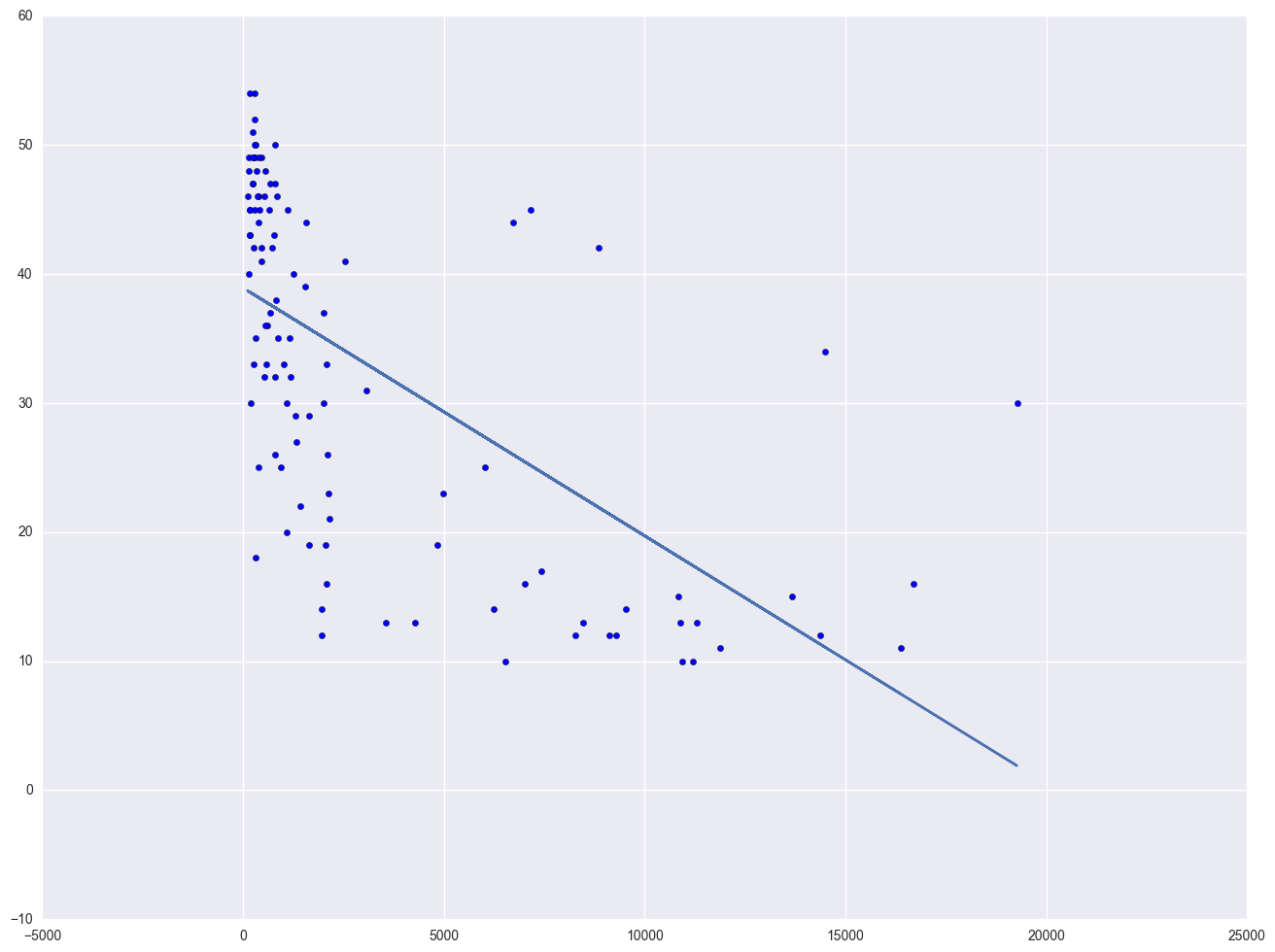

Let's look at the relationship between GNP per capita (gnpcap) and births (birth). Below if we look at the scatterplot between gnpcap and birth, we can see that the relationship between these two variables is quite non-linear. We added a regression line to the chart, and you can see how poorly the line fits this data. Also, if we look at the residuals by predicted plot, we see that the residuals are not nearly homoscedastic, due to the non-linearity in the relationship between gnpcap and birth.

nations = pd.read_csv(mypath + "nations.csv")

# print nations.describe()

lm = smf.ols(formula = "birth ~ gnpcap", data = nations).fit()

print lm.summary()

plt.scatter(lm.predict(), lm.resid)

plt.show()

plt.scatter(nations.gnpcap, nations.birth)

plt.plot(nations.gnpcap, lm.params[0] + lm.params[1] * nations.gnpcap, '-')

plt.show()

OLS Regression Results

==============================================================================

Dep. Variable: birth R-squared: 0.392

Model: OLS Adj. R-squared: 0.387

Method: Least Squares F-statistic: 69.05

Date: Mon, 26 Dec 2016 Prob (F-statistic): 3.27e-13

Time: 15:42:45 Log-Likelihood: -411.80

No. Observations: 109 AIC: 827.6

Df Residuals: 107 BIC: 833.0

Df Model: 1

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [95.0% Conf. Int.]

------------------------------------------------------------------------------

Intercept 38.9242 1.261 30.856 0.000 36.423 41.425

gnpcap -0.0019 0.000 -8.309 0.000 -0.002 -0.001

==============================================================================

Omnibus: 1.735 Durbin-Watson: 1.824

Prob(Omnibus): 0.420 Jarque-Bera (JB): 1.335

Skew: -0.011 Prob(JB): 0.513

Kurtosis: 2.458 Cond. No. 6.73e+03

==============================================================================

Warnings:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

[2] The condition number is large, 6.73e+03. This might indicate that there are

strong multicollinearity or other numerical problems.

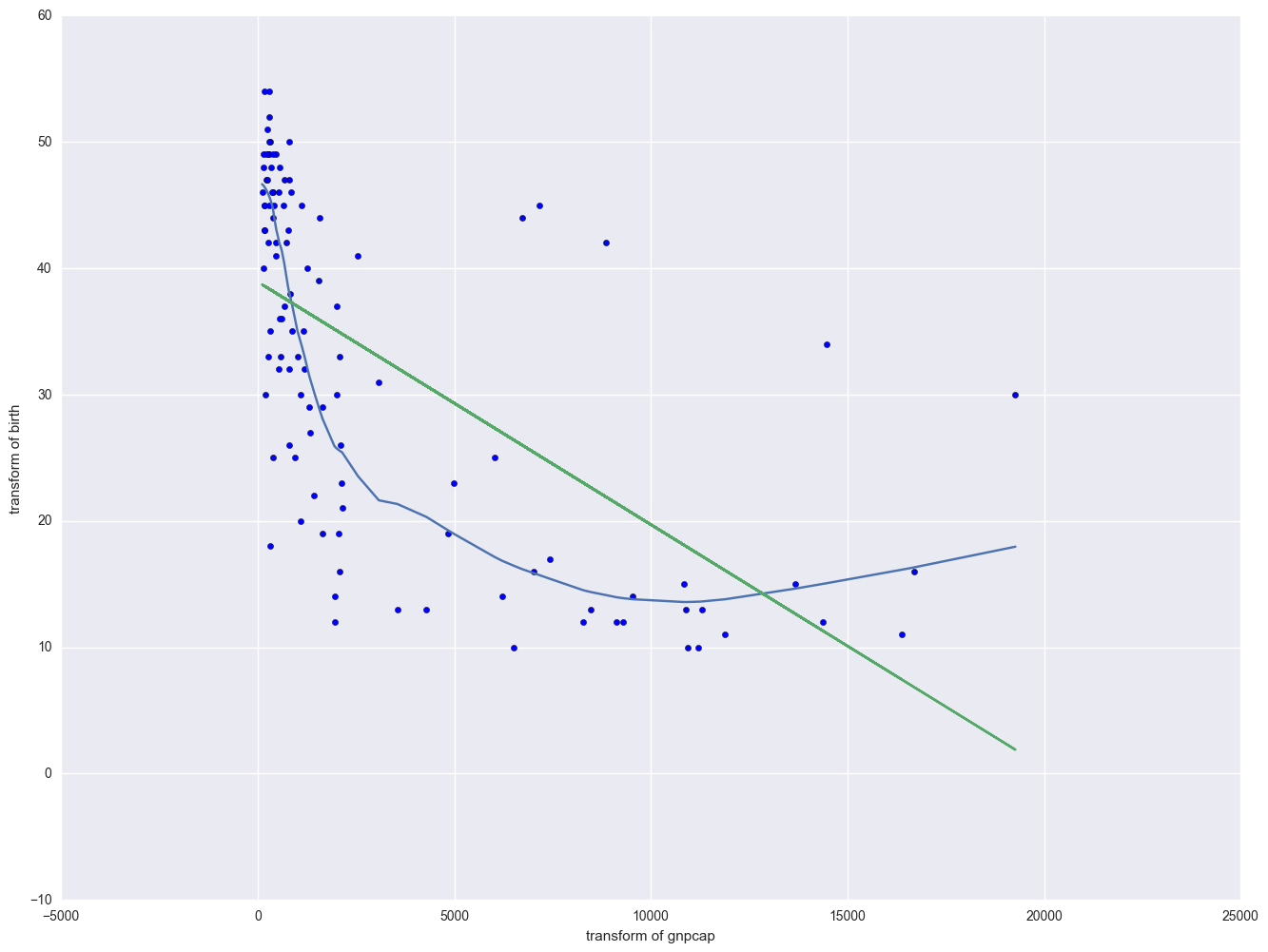

Now we are going to modify the above scatterplot by adding a lowess (also called "loess") smoothing line. We show only the graph with the 0.4 smooth.

from statsmodels.nonparametric.smoothers_lowess import lowess

lowess_df = pd.DataFrame(lowess(endog = nations.birth, exog = nations.gnpcap, frac = 0.4), columns = ["gnpcap", "birth"])

plt.plot(lowess_df.gnpcap, lowess_df.birth)

plt.scatter(nations.gnpcap, nations.birth)

plt.plot(nations.gnpcap, lm.params[0] + lm.params[1] * nations.gnpcap, '-')

plt.xlabel("transform of gnpcap")

plt.ylabel("transform of birth")

plt.show()

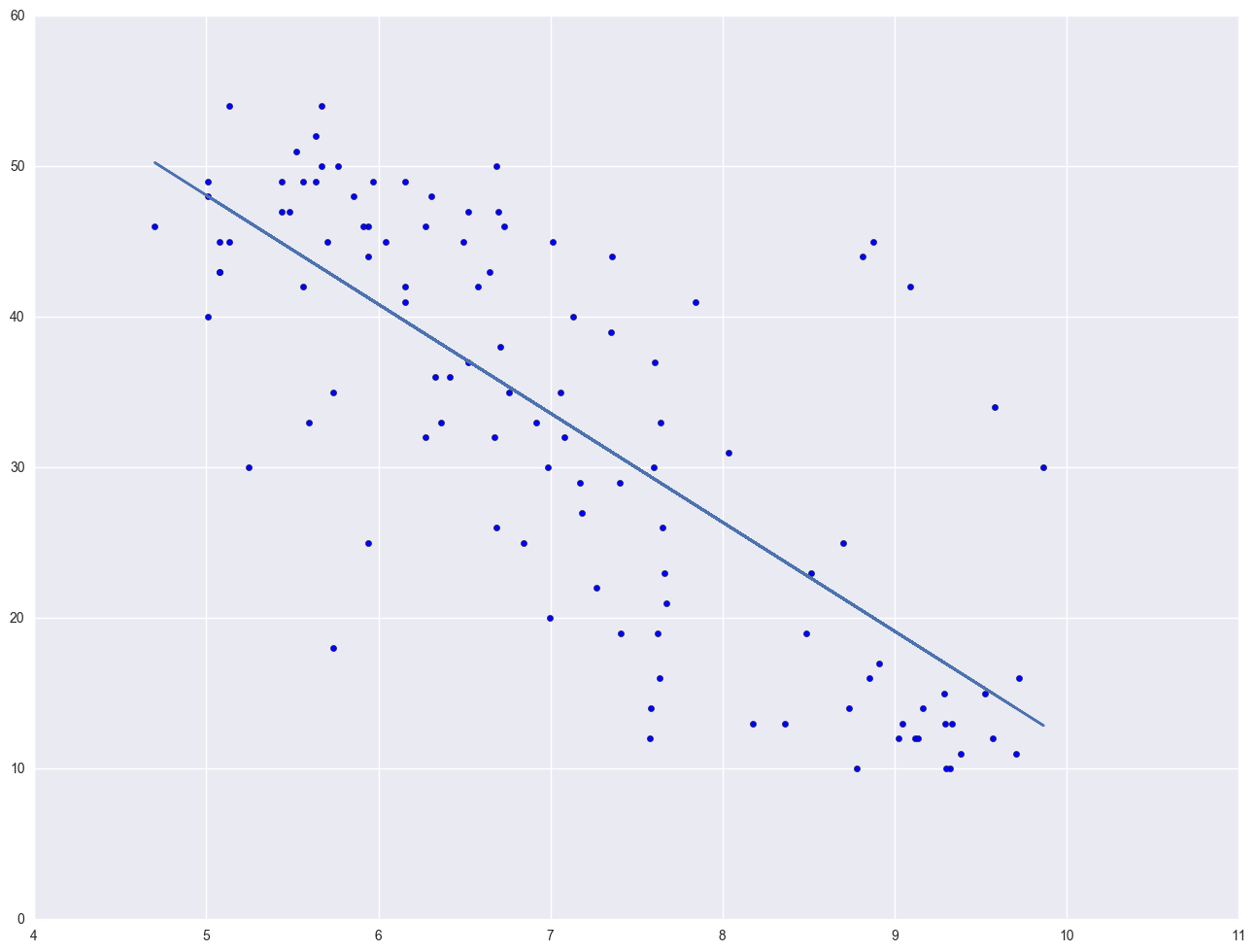

The lowess line fits much better than the OLS linear regression. In trying to see how to remedy these, we notice that the gnpcap scores are quite skewed with most values being near 0, and a handful of values of 10,000 and higher. This suggests to us that some transformation of the variable may be useful. One of the commonly used transformations is a log transformation. Let's try it below. As you see, the scatterplot between lgnpcap and birth looks much better with the regression line going through the heart of the data. Also, the plot of the residuals by predicted values look much more reasonable.

nations["log_gnpcap"] = nations.gnpcap.map(lambda x: math.log(x))

lm2 = smf.ols("birth ~ log_gnpcap", data = nations).fit()

print lm2.summary()

plt.scatter(lm2.predict(), lm2.resid)

plt.show()

plt.scatter(nations.log_gnpcap, nations.birth)

plt.plot(nations.log_gnpcap, lm2.params[0] + lm2.params[1] * nations.log_gnpcap, '-')

plt.show()

OLS Regression Results

==============================================================================

Dep. Variable: birth R-squared: 0.571

Model: OLS Adj. R-squared: 0.567

Method: Least Squares F-statistic: 142.6

Date: Mon, 26 Dec 2016 Prob (F-statistic): 2.12e-21

Time: 16:08:02 Log-Likelihood: -392.77

No. Observations: 109 AIC: 789.5

Df Residuals: 107 BIC: 794.9

Df Model: 1

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [95.0% Conf. Int.]

------------------------------------------------------------------------------

Intercept 84.2773 4.397 19.168 0.000 75.561 92.993

log_gnpcap -7.2385 0.606 -11.941 0.000 -8.440 -6.037

==============================================================================

Omnibus: 2.875 Durbin-Watson: 1.790

Prob(Omnibus): 0.237 Jarque-Bera (JB): 2.267

Skew: 0.282 Prob(JB): 0.322

Kurtosis: 3.425 Cond. No. 37.8

==============================================================================

Warnings:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

This section has shown how you can use scatterplots to diagnose problems of non-linearity, both by looking at the scatterplots of the predictor and outcome variable, as well as by examining the residuals by predicted values. These examples have focused on simple regression; however, similar techniques would be useful in multiple regression. However, when using multiple regression, it would be more useful to examine partial regression plots instead of the simple scatterplots between the predictor variables and the outcome variable.

2.6 Model Specification

A model specification error can occur when one or more relevant variables are omitted from the model or one or more irrelevant variables are included in the model. If relevant variables are omitted from the model, the common variance they share with included variables may be wrongly attributed to those variables, and the error term is inflated. On the other hand, if irrelevant variables are included in the model, the common variance they share with included variables may be wrongly attributed to them. Model specification errors can substantially affect the estimate of regression coefficients.

Consider the model below. This regression suggests that as class size increases the academic performance increases. Before we publish results saying that increased class size is associated with higher academic performance, let's check the model specification.

elemapi2_0 = elemapi2[~np.isnan(elemapi2.acs_k3)]

lm = smf.ols("api00 ~ acs_k3", data = elemapi2_0).fit()

elemapi2_0.loc[:, "fv"] = lm.predict()

elemapi2_0.loc[:, "fvsquare"] = elemapi2_0.fv ** 2

There are a couple of methods to detect specification errors. A link test performs a model specification test for single-equation models. It is based on the idea that if a regression is properly specified, one should not be able to find any additional independent variables that are significant except by chance. To conduct this test, you need to obtain the fitted values from your regression and the squares of those values. The model is then refit using these two variables as predictors. The fitted value should be significant because it is the predicted value. One the other hand, the fitted values squared shouldn't be significant, because if our model is specified correctly, the squared predictions should not have much of explanatory power. That is, we wouldn't expect the fitted value squared to be a significant predictor if our model is specified correctly. So we will be looking at the p-value for the fitted value squared.

lm = smf.ols("api00 ~ fv + fvsquare", data = elemapi2_0).fit()

print lm.summary()

OLS Regression Results

==============================================================================

Dep. Variable: api00 R-squared: 0.035

Model: OLS Adj. R-squared: 0.030

Method: Least Squares F-statistic: 7.089

Date: Tue, 27 Dec 2016 Prob (F-statistic): 0.000944

Time: 14:52:59 Log-Likelihood: -2529.9

No. Observations: 398 AIC: 5066.

Df Residuals: 395 BIC: 5078.

Df Model: 2

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [95.0% Conf. Int.]

------------------------------------------------------------------------------

Intercept 3884.5065 2617.696 1.484 0.139 -1261.853 9030.866

fv -11.0501 8.105 -1.363 0.174 -26.984 4.883

fvsquare 0.0093 0.006 1.488 0.138 -0.003 0.022

==============================================================================

Omnibus: 135.464 Durbin-Watson: 1.420

Prob(Omnibus): 0.000 Jarque-Bera (JB): 20.532

Skew: 0.048 Prob(JB): 3.48e-05

Kurtosis: 1.891 Cond. No. 1.58e+08

==============================================================================

Warnings:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

[2] The condition number is large, 1.58e+08. This might indicate that there are

strong multicollinearity or other numerical problems.

Let's try adding one more variable, meals, to the above model and then run the link test again.

lm = smf.ols("api00 ~ acs_k3 + full + fv", data = elemapi2_0).fit()

print lm.summary()

OLS Regression Results

==============================================================================

Dep. Variable: api00 R-squared: 0.339

Model: OLS Adj. R-squared: 0.335

Method: Least Squares F-statistic: 101.2

Date: Tue, 27 Dec 2016 Prob (F-statistic): 3.29e-36

Time: 14:54:29 Log-Likelihood: -2454.6

No. Observations: 398 AIC: 4915.

Df Residuals: 395 BIC: 4927.

Df Model: 2

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [95.0% Conf. Int.]

------------------------------------------------------------------------------

Intercept -0.3727 0.515 -0.724 0.469 -1.384 0.639

acs_k3 6.4796 8.922 0.726 0.468 -11.060 24.020

full 5.3898 0.396 13.598 0.000 4.611 6.169

fv 0.1057 0.271 0.390 0.697 -0.427 0.639

==============================================================================

Omnibus: 15.537 Durbin-Watson: 1.367

Prob(Omnibus): 0.000 Jarque-Bera (JB): 7.217

Skew: -0.017 Prob(JB): 0.0271

Kurtosis: 2.341 Cond. No. 9.77e+17

==============================================================================

Warnings:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

[2] The smallest eigenvalue is 1.79e-28. This might indicate that there are

strong multicollinearity problems or that the design matrix is singular.

The link test is once again non-significant. Note that after including meals and full, the coefficient for class size is no longer significant. While acs_k3 does have a positive relationship with api00 when no other variables are in the model, when we include, and hence control for, other important variables, acs_k3 is no longer significantly related to api00 and its relationship to api00 is no longer positive.

2.7 Issues of Independence

The statement of this assumption is that the errors associated with one observation are not correlated with the errors of any other observation cover several different situations. Consider the case of collecting data from students in eight different elementary schools. It is likely that the students within each school will tend to be more like one another that students from different schools, that is, their errors are not independent. We will deal with this type of situation in Chapter 4.

Another way in which the assumption of independence can be broken is when data are collected on the same variables over time. Let's say that we collect truancy data every semester for 12 years. In this situation it is likely that the errors for observation between adjacent semesters will be more highly correlated than for observations more separated in time. This is known as autocorrelation. When you have data that can be considered to be time-series, you should use the dw option that performs a Durbin-Watson test for correlated residuals.

We don't have any time-series data, so we will use the elemapi2 dataset and pretend that snum indicates the time at which the data were collected. We will sort the data on snum to order the data according to our fake time variable and then we can run the regression analysis with the dw option to request the Durbin-Watson test. The Durbin-Watson statistic has a range from 0 to 4 with a midpoint of 2. The observed value in our example is less than 2, which is not surprising since our data are not truly time-series.

lm = smf.ols(formula = "api00 ~ enroll", data = elemapi2).fit()

print lm.summary()

print "Durbin-Watson test statistics is " + str(stools.durbin_watson(lm.resid))

plt.scatter(elemapi2.snum, lm.resid)

plt.show()

OLS Regression Results

==============================================================================

Dep. Variable: api00 R-squared: 0.101

Model: OLS Adj. R-squared: 0.099

Method: Least Squares F-statistic: 44.83

Date: Tue, 27 Dec 2016 Prob (F-statistic): 7.34e-11

Time: 15:00:28 Log-Likelihood: -2528.8

No. Observations: 400 AIC: 5062.

Df Residuals: 398 BIC: 5070.

Df Model: 1

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [95.0% Conf. Int.]

------------------------------------------------------------------------------

Intercept 744.2514 15.933 46.711 0.000 712.928 775.575

enroll -0.1999 0.030 -6.695 0.000 -0.259 -0.141

==============================================================================

Omnibus: 43.040 Durbin-Watson: 1.342

Prob(Omnibus): 0.000 Jarque-Bera (JB): 17.113

Skew: 0.277 Prob(JB): 0.000192

Kurtosis: 2.152 Cond. No. 1.26e+03

==============================================================================

Warnings:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

[2] The condition number is large, 1.26e+03. This might indicate that there are

strong multicollinearity or other numerical problems.

Durbin-Watson test statistics is 1.34234658795

2.8 Summary

In this chapter, we have used a number of tools in SAS for determining whether our data meets the regression assumptions. Below, we list the major commands we demonstrated organized according to the assumption the command was shown to test.

Detecting Unusual and Influential Data

scatterplots of the dependent variables versus the independent variable

looking at the largest values of the studentized residuals, leverage, Cook's D, DFFITS and DFBETAs

Tests for Normality of Residuals Tests for Heteroscedasity

kernel density plot

quantile-quantile plots

standardized normal probability plots

Shapiro-Wilk W test

scatterplot of residuals versus predicted (fitted) values

White test

Tests for Multicollinearity

looking at VIF

looking at tolerance

Tests for Non-Linearity

scatterplot of independent variable versus dependent variable

Tests for Model Specification

time series

Durbin-Watson test

reference

- Interpreting plot.lm()

- statsmodels.stats.outliers_influence.OLSInfluence

- Regression Diagnostics and Specification Tests

- Statistics stats

- lowess smoothing

- outlier influence

from statsmodels.stats.outliers_influence import OLSInfluence

print pd.Series(OLSInfluence(lm).influence, name = "Leverage")